Seed/Grain Traders in Ethiopia Provide Key Insights on Seed Supply and Prices

This week we continue our series on the latest Seed System Security Assessment, which was conducted in Ethiopia in September/October 2016, where the consequences of the most severe drought in decades are still unfolding. The assessment– which is designed to help development managers and field staff assess whether interventions in seed systems are needed– included a survey of nearly 500 households, interviews with about 50 seed/grain traders, and multiple community meetings and key informant sessions. Learn more about SSSAs.

In our post last week, we reported that while 70% of farmers surveyed in the SSSA indicated they sowed less than usual during the 2016 Meher (primary cropping season), only 1.3% indicated seed was not available locally.

But these were not the only findings suggesting the seed security situation in Ethiopia remains relatively stable.

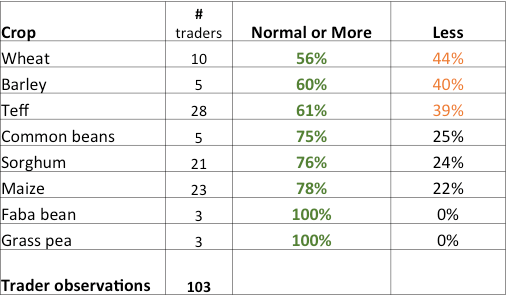

If seed availability were a constraint, we would expect seed supply to decline, and seed prices to rise steeply. Here, the evidence from the SSSA presents a nuanced picture. For each major crop, the majority of seed traders interviewed indicated the seed supply as being either normal or more than usual.

Traders’ Assessment of Seed Supply for Meher 2016

In addition, traders indicated only a modest (+18%) average increase in seed prices across all crops. This puts traders’ views on seed supply shifts into perspective – while 18% is not an immaterial increase, it is also not alarming.

Analyzing price changes by crop may be more useful for practitioners designing seed system interventions. For example, while sorghum rose 27% and teff rose 23% in price from last season, wheat’s price fell by 3%. Overall these prices hikes may fall within a range of normal variation, and do not necessarily signal extreme stress.